Debt… it sucks, to put it lightly. I’m sure you are painfully aware of how much debt you have, but do you know how much that debt balance is costing you each day?

It turns out it could be a lot.

The majority of Americans have debt, but not all debt is the same.

Taking on debt to get a college degree is “good” debt because that will eventually lead to a higher income throughout your life.

But, racking up the debt for a trip to Maui or Cancun with your squad is often considered “bad” debt.

We aren’t going to get into the finer details of debt in this post, but take a deeper dive on what debt is and why it isn’t evil, by checking out our recent post.

How Your Debt Costs You Money

Did you know that regardless of “good” or “bad”, your debt costs you money every day?

When you carry a balance on your credit card or your student loan debt, interest continues to accrue over a certain time period.

This can be monthly, daily, or even continuously!

Most personal debt accrues interest daily or continuously (it’s not as much as you think, but still not great) because interest is required to be paid before the balance is paid.

Let’s get into the math of how this all works.

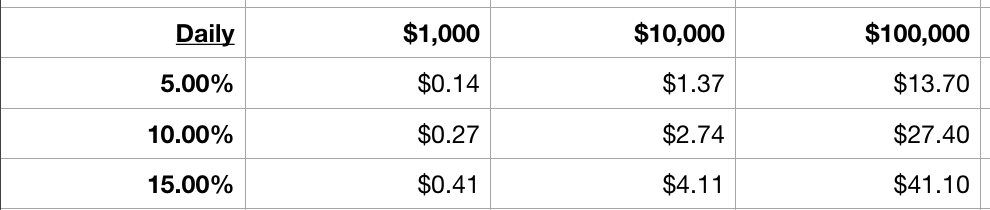

Here is a table of the daily cost of different balances of debt at varying interest rates:

Interest rates can differ quite a bit between each person and circumstance. But, to give you a sense of the different rate breakouts, here are what the interest rates are for:

- 5% is a rate that you might see for a home mortgage or student loans

- 10% is a rate that you might see for a personal line of credit or personal loan

- 15% is a rate that you might see for a credit card

As you can see, at the $1,000 amount the daily cost isn’t that much. But, over a longer period of time and higher amounts, the costs can start to add up.

Example of How Debt Costs You Money

Let’s look at a specific example to get an even better sense of just how much your debt can cost you.

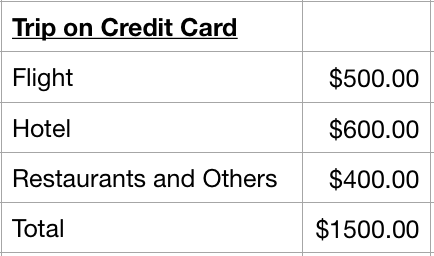

Example: 3-Day Trip

In this example, let’s imagine that you take that 3-day trip to Maui with your friends.

Here are the basic costs:

Now, what happens if you decide to put this trip on a credit card?

Let’s imagine you pay $200 each month on the trip:

If you didn’t let the table of numbers scare you, you will see that the trip ended up costing you $1,564.50 instead of just $1,500.

While this may not seem like a lot of additional money, it can quickly add up.

And while we only looked at this example, it is easy to rack up the interest debt on a number of expenses in your life that you might not always consider.

You must be mindful of the true costs of your purchases and resulting debt that you’ll need to pay.

Let’s look at what would happen if you only paid off $100 of the balance each month:

That $1,500 trip ends up costing you a whopping $1,648.73. Basically it could take you almost 2.5 years to payoff the Maui trip!

Looks like that little getaway just won’t leave you alone. And honestly, with everything else you have going on, this is not something you want to take on.

Final Thoughts

Listen, we’re not saying that you shouldn’t use credit, but we are highly encouraging you to be mindful of the true cost of those purchases.

At the end of the day, carrying debt balances costs you additional money.

It’s crucial that you plan out your credit purchases so you can avoid this additional cost.

Take a minute to look at your own financial situation today.

If you were to take that Maui trip from the example and put it on your credit card, how much would you be able to realistically pay each month on top of your other necessary monthly expenses?

Don’t you think it would be better to delay the trip and save up until you have the funds? For more on budgeting, check out our post here.

P.S. If you liked this post and are interested in figuring out your financial situation, sign up for our weekly newsletter! We provide exclusive tips and advice to help you get on the best financial path for your lifestyle.

Leave a Reply

Your email is safe with us.

You must be logged in to post a comment.